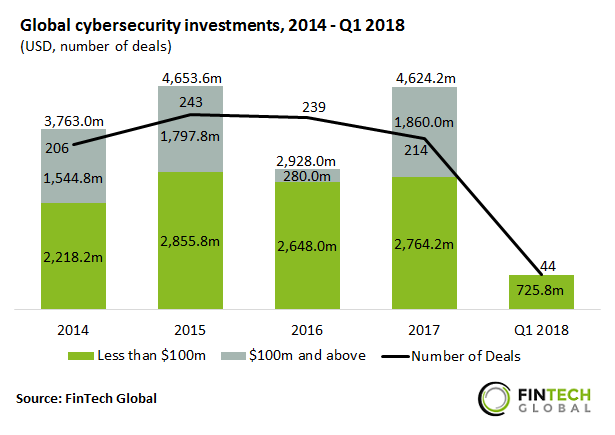

Capital invested in the first quarter of this year declined by half compared to Q4 2017

- Total investment in Q1 2018 reached just $725.8m, a fall of 47.7% from the previous quarter. However, compared to the same quarter in 2017, total funding increased by 27%.

- The drop in investment in Q1 2018 can be attributed to a lack of later-stage deals valued above $100m. There were three such deals during the previous quarter, the largest of which was a $500m strategic investment in Symantec, a provider of security software and systems management solutions, from Silver Lake Partners.

- When interval analysis is applied investments valued under $100m actually increased by 30.3% in Q1 2018 compared to the previous quarter.

- Despite the decrease in total funding, deal activity increased for the first time in four quarters with a total of 44 deals closed.

Global cybersecurity investments make a slow start to the year

- The $725.8m invested in Q1 2018 equates to just 15.7% of last year’s total funding. Thus, if investment continues at this pace, it is not projected to surpass 2017’s total. However, investment was similarly slow at the beginning of 2017 and gained momentum later in the year.

- The largest cybersecurity deal so far this year was a $75m investment in Ledger, a developer of cybersecurity solutions for cryptocurrency and blockchain applications. The Series B round was led by Draper Esprit with co-investment from Digital Currency Group and CapHorn Invest, among others.

- Deal activity was also slightly behind pace in Q1, standing at 44 deals which represents 20.6% of the total number of deals closed during 2017. That figure stood at 67 deals at the end of Q1 2017.

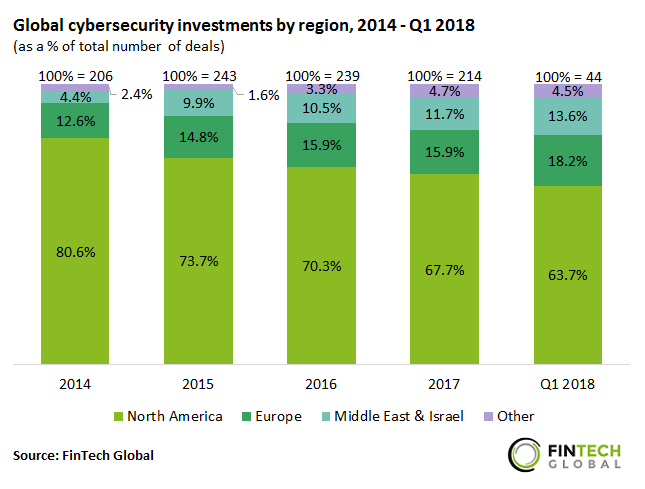

Investors are increasingly backing companies based outside of the US

- Between 2014 and 2017, North America’s share of deals dropped by 12.9 percentage points (pp) from 80.6% to 67.7%. This share further decreased in Q1 2018 reaching 63.7%.

- This was mainly offset by an increase in deal share in both Europe and the Middle East & Israel. Europe’s share of deals increased from 12.6% in 2014 to 15.9% in 2017. This trend continued in Q1 2018 to reach 18.2%.

- Similarly, the Middle East & Israel’s share of deals jumped from 4.4% in 2014 to 11.7% in 2017. This value reached 13.6% in Q1 2018, more than triple the original value.

- The growing cybersecurity hub in Israel is the catalyst for this shift. Israel has developed a strong cybersecurity ecosystem that encourages collaboration between the government (including the military), private sector organizations and universities.

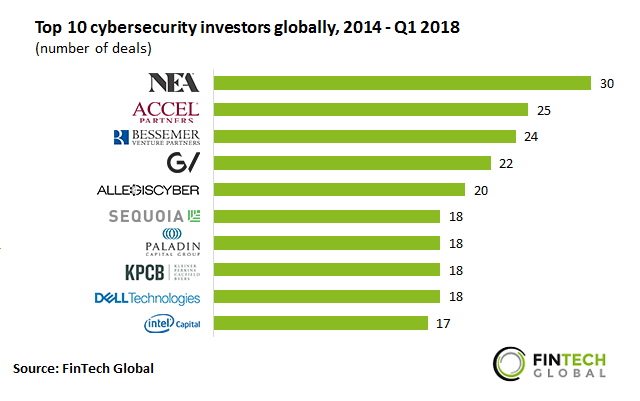

US venture capital firms and corporate VCs are the top backers of cybersecurity companies

- The ten most active investors in the cybersecurity sector between 2014 and Q1 2018 are all headquartered in the US. The list is comprised of seven venture capital firms, as well as the investment arms of three corporates: Google, Dell and Intel.

- New Enterprise Associates (NEA), a Menlo Park-based VC firm, was the most active investor over this period with 30 investments. The largest deal that NEA participated in was a $110m investment in Cloudflare, a web performance and security company, in Q3 2015.

- Accel Partners followed with 25 investments. Accel’s portfolio includes some of the most well-funded cybersecurity companies including Tenable, Illumio and CrowdStrike.

The data for this research was taken from the FinTech Global database. More in-depth data and analytics on investments and companies across all FinTech sectors and regions around the world are available to subscribers of FinTech Global. ©2018 FinTech Global

Copyright © 2018 RegTech Analyst